The client's task

Title

Tax residency analysis

Description

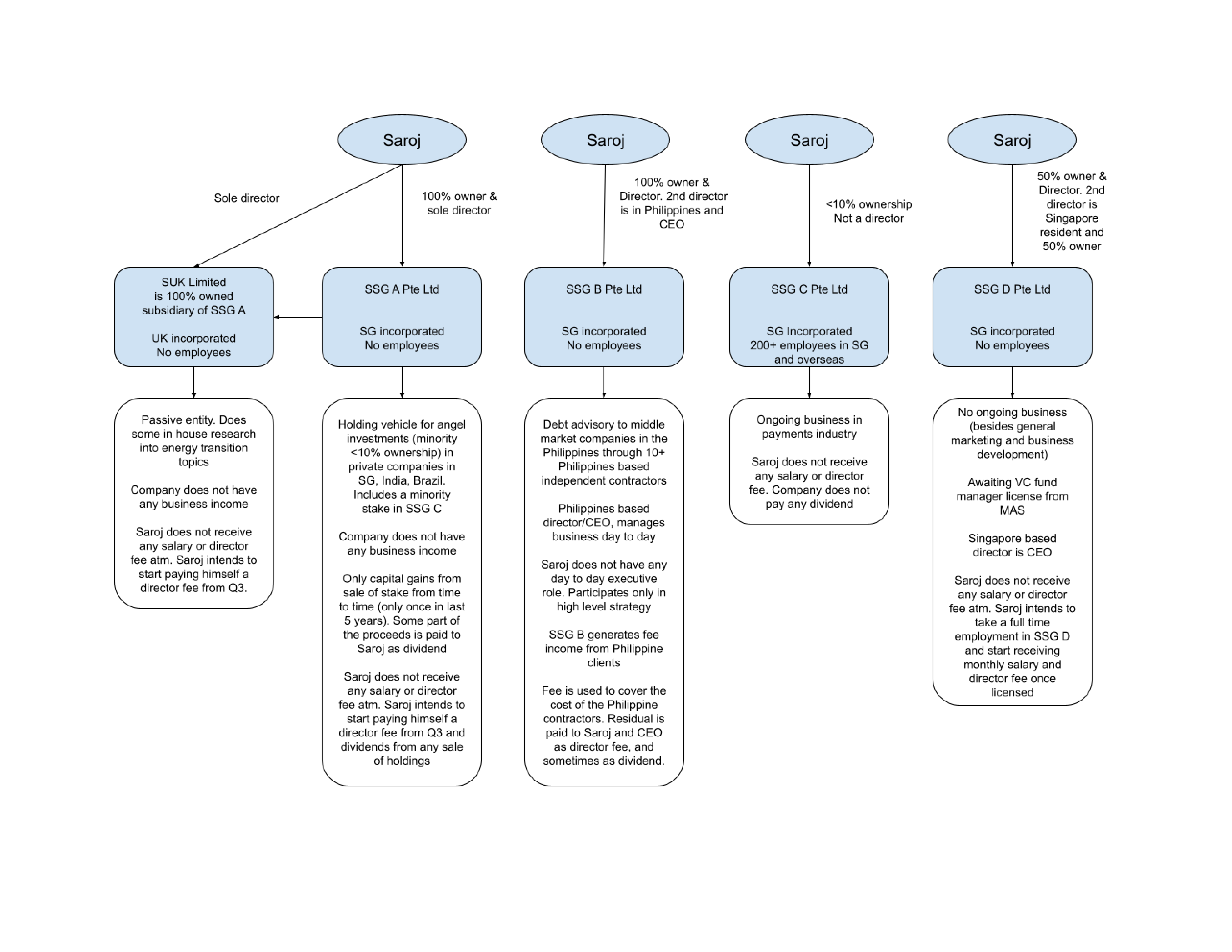

I am based in UK but have ownership and involvement in several Singapore based companies.

Need to understand the tax residency classification of those companies.

Tax residency analysis

I am based in UK but have ownership and involvement in several Singapore based companies.

Need to understand the tax residency classification of those companies.

It is a UK tax resident by its place of incorporation.

A)A is a UK tax resident under its domestic law.

For companies incorporated outside the UK, residency is determined by the Central Management and Control (CMC) test.

As you are the sole director making all strategic decisions from the UK, HMRC will conclude that the company's CMC is exercised in the UK.

A is not a tax resident of Singapore.

Similarly to the UK, Singapore applies the CMC test.

As A does not have any employees in Singapore, and the sole director is based in the UK, the Inland Revenue Authority of Singapore (IRAS) will not consider that the CMC is exercised in Singapore.

B)The Philippines determines corporate tax residency by the place of incorporation, not the Place of Effective Management (POEM), so B a not a Philippines tax resident.

B must pay tax in the Philippines on its local income as a foreign corporation.

The Philippines law will still use the term «resident» for B within the concept of a «resident foreign corporation», but this does not constitute tax residency.

There is a significant risk of B being deemed a UK tax resident.

Your 100% ownership and directorship allow you to exert decisive influence.

Point 7 below describes how to mitigate this risk.

The grounds for residency in Singapore are weak.

The company is incorporated in Singapore but has no employees there.

Furthermore, the day-to-day management and operational activities (working with clients in the Philippines) are carried out by the second director, the CEO, who is based in the Philippines.

C)It is a Singapore tax resident based on its significant local operations and management.

No UK residency risk exists as you lack authority for central management and control.

D)D is a Singapore tax resident under the **UK/Singapore Double Taxation Agreement **(DTA), as its POEM is determined by the key role of the Singapore-based director and CEO.

However, a high risk of it also being deemed a UK resident exists (point 5.5) and must be mitigated (point 7).

Grounds for Singapore residency are strong: the second director is an Singapore-resident CEO owning 50%, and the company awaits a MAS (Monetary Authority of Singapore) licence, showing close regulatory and operational ties to Singapore.

The presence in Singapore of a CEO responsible for operations and obtaining a MAS license is decisive.

A CEO typically has a more significant role in key commercial decisions than a non-executive director abroad.

Your plan to relocate to Singapore for full-time work in D is a compelling argument that the company's strategic management is and will remain in Singapore.

This plan strengthens the Singapore-based CEO's current role and confirms the company's management is focused on Singapore.

Your 50% ownership and directorship in D create a high risk of it being deemed a UK tax resident.

This equal split of shares and board seats can create divided management, which under UK case law may lead to dual residency.

Point 7 below describes how to mitigate this risk.

Your current corporate structure is highly risky:

A, B, and D face a high risk of being deemed tax residents in both the UK (due to your centralised control) and their country of incorporation or operation.

UK tax authorities might view your activities across these companies collectively, asserting a consistent pattern of management from the UK.

You must prove each board acts independently.

If one company is deemed a UK resident, the risk extends to the others.

Even if B and D are non-resident in the UK under the DTA, your UK activities are highly likely to create a Dependent Agent Permanent Establishment (DAPE), resulting in a UK corporation tax liability on profits attributable to it.

To mitigate the risks of points 3.2, 5.5, and 6, I recommend:

Appoint additional, independent Singapore-resident directors.

Limit your role to a non-executive one.

For B and D, the corporate documents must clearly state that the CEOs (in the Philippines and Singapore) are responsible for day-to-day management and key commercial decisions.

Implement strict protocols for board of directors' meetings to ensure that strategic decisions are made outside the UK:

The majority (ideally, all) of board meetings must be physically held in the intended country of residence (Singapore, the Philippines).

A quorum must be constituted without the participation of directors located in the UK.

Remote meetings participation from the UK weakens your position.

Maintain detailed minutes showing genuine discussion and decision-making, as this is a critical defence element.

Avoid making strategic decisions through informal emails or calls from the UK.

Limit your role to strategic oversight as a shareholder/non-executive director.

Delegate contractual authority for B and D to the CEOs in the Philippines and Singapore.

Avoid UK activities that could be construed as concluding contracts for the Singapore companies.